Most products on this page are from partners who may compensate us. This may influence which products we write about and where and how they appear on the page. However, opinions expressed here are the author's alone, not those of any bank, credit card issuer, airline or hotel chain.

What Is a Good Credit Score?

iStock

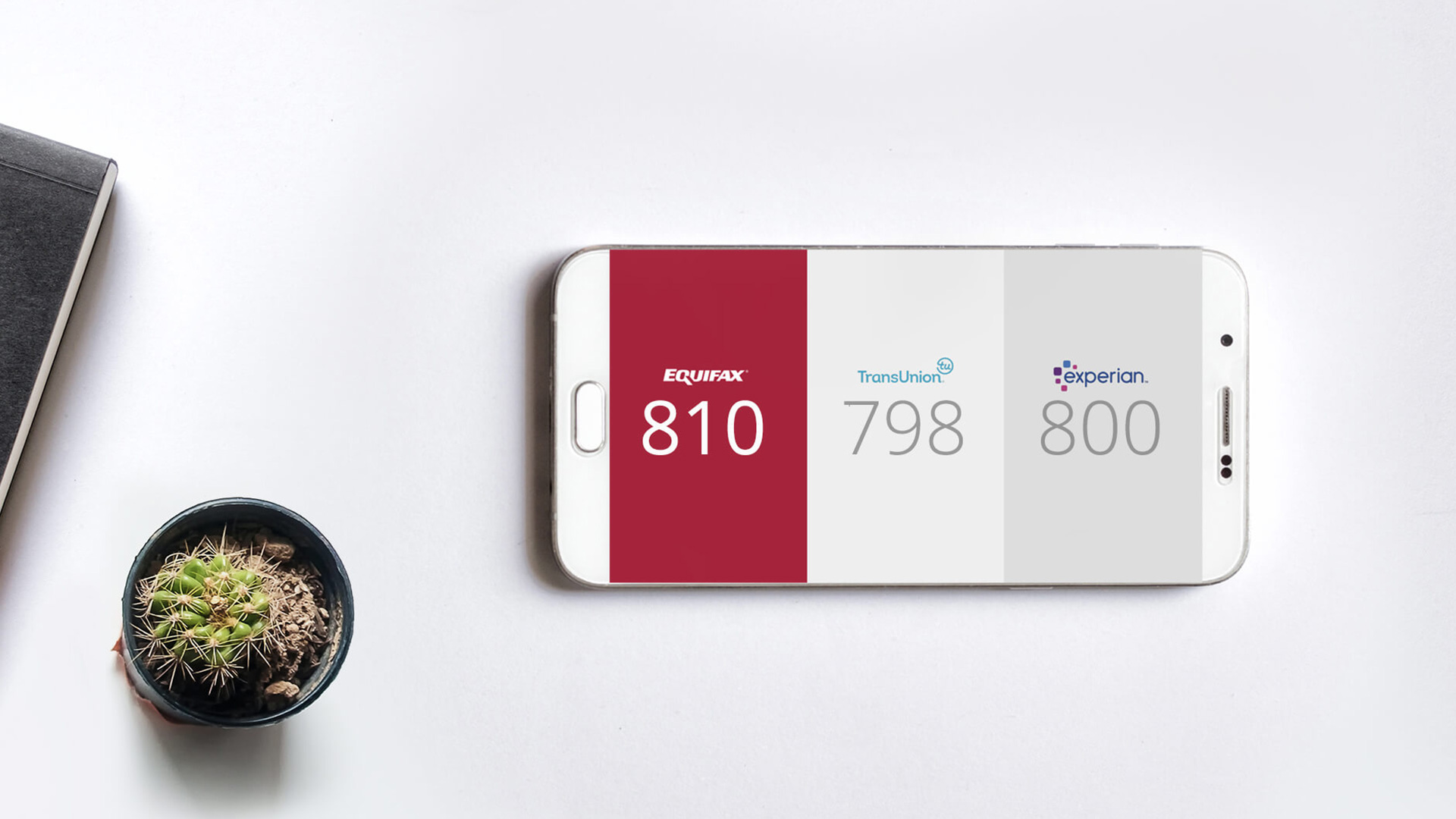

According to the credit bureau Experian, 67% of American adults have a good

1. Lower Interest Rates

A good credit score not only makes it easier to qualify for credit cards and loans, but it could help you qualify for more attractive financing offers as well. In general, lenders and credit card companies reserve their

You typically don’t need a perfect credit score to qualify for the best deals that credit card issuer and lenders have to offer. But with good or excellent credit, you’re more likely to be eligible for a wider variety of financing options—including 0% APR credit card offers and premium credit cards if you’re interested in such pro

2. Higher Credit Limits

When you qualify for a new credit card, the card issuer may also review your credit score to determine how much money it’s comfortable allowing you to borrow at a given time (aka your credit limit). A good credit score could give you access to

On a positive note, if you start out with credit cards with lower limits you can work to

3. Better Credit Card Offers and Loans

Credit card companies and lenders commonly set criteria that applicants must meet to borrow money. Satisfying a minimum credit score is typically part of the pro

For example, the

Recommended Travel Credit Cards

| Credit Card | Intro Bonus | Annual Fee | Rewards Rate | Learn More |

|---|---|---|---|---|

|

|

60,000Chase Ultimate Rewards Points

Earn 60,000 bonus points after you spend $4,000 on purchases in the first 3 months from account opening. Dollar Equivalent: $1,380 (60,000 Chase Ultimate Rewards Points * 0.023 base) |

$95 |

1x- 5xPoints

The card offers 5x points per dollar on Chase Travel℠, 3x points on dining (including eligible takeout and delivery services), as well as 3x points on select streaming services and online grocery purchases (excluding Target, Walmart and wholesale clubs). This card earns 2x points on all other travel spending and 1x point per dollar everywhere else. Chase broadly defines travel to include not just airfare, hotels and rental cars, but expenses like parking, tolls and public transit too. |

Apply Now |

|

|

50,000Southwest Rapid Rewards Points

Earn 50,000 bonus points after spending $1,000 on purchases in the first 3 months from account opening. Dollar Equivalent: $700 (50,000 Southwest Rapid Rewards Points * 0.014 base) |

$69 |

1x - 2xPoints

Earn 2X points on Southwest® purchases. Earn 2X points on Rapid Rewards® hotel and car rental partners. Earn 2X points on local transit and commuting, including rideshare. Earn 2X points on internet, cable, and phone services; select streaming. Earn 1X points on all other purchases. |

Apply Now |

|

|

$200Cash Bonus

Earn $200 in cash back after you spend $1500 on purchases in the first 6 months of account opening. This bonus offer will be fulfilled as 20,000 ThankYou® points, which can be redeemed for $200 cash back. |

$0 |

1% - 5%Cashback

Earn 5% cash back on purchases in your top eligible spend category each billing cycle, up to the first $500 spent, 1% cash back thereafter. Also, earn unlimited 1% cash back on all other purchases. Special Travel Offer: Earn an additional 4% cash back on hotels, car rentals, and attractions booked on Citi Travel℠ portal through 6/30/2025. |

Apply Now Rates & Fees |

|

|

60,000Citi ThankYou Points

Earn 60,000 bonus ThankYou Points after making $4,000 worth of purchases during the first three months of account opening. Dollar Equivalent: $1,080 (60,000 Citi ThankYou Points * 0.018 base) |

$95 |

1X-10XPoints

10X total ThankYou® Points per $1 spent on hotel, car rentals and attractions (excluding air travel) booked on the Citi Travel℠ portal through June 30, 2024. 3X -- Earn 3 Points per $1 spent at Gas Stations, Air Travel and Other Hotels 3X -- Earn 3 Points per $1 spent at Restaurants and Supermarkets 1X -- Earn 1 Point on All Other Purchases |

Apply Now Rates & Fees |

Other lenders may also use credit score minimums to screen loan applicants. The

4. Lower Insurance Premiums

Another perk of good credit that many people overlook is the potential to save money on your insurance rates. In many states, the price of your car insurance and homeowners insurance may go up or

Many insurance companies use credit-based insurance scores to assess risk when providing quotes to potential customers. Your credit information can help an insurer determine the likelihood that you’ll file a claim in the future—a claim that could cost the

Insurance companies place a lot of trust in the predictive power of credit scores. You might have a completely clean driving record. However, if you have a bad credit score, you could still pay a higher insurance rate than you would otherwise. One

5. More Housing Choices

Whether you decide to rent an apartment, lease a home, or apply for a mortgage, your credit score is likely to come into play in each scenario. Landlords and property managers typically review the credit history and credit score of

Good credit can make securing housing easier and more affordable whether you decide to rent or buy. Down payment and security deposit requirements are often lower for applicants with higher credit scores. Plus, you’ll need to satisfy minimum credit score requirements to qualify for a mortgage or to lease an apartment in the

Related Article

Related Article

Apartment Hunting Tips If You Have Bad Credit

Next Steps

Equifax

Good credit can save you money and make your financial life easier to navigate in many ways. So, if your credit score isn’t as strong as you would like it to be, it’s in your best interest to take action.

If you want to

Another possible way to boost your credit scores is to

Depending on your situation, the changes above (and others) may not help you

Michelle Lambright Black

Michelle Black is founder of CreditWriter.com and HerCreditMatters.com. Michelle is a leading credit card journalist with over a decade and a half of experience in the financial industry. She’s an expert on credit reporting, credit scoring, identity theft, budgeting, small business, and debt eradication. Michelle is also a certified credit expert witness and personal finance writer.