Most products on this page are from partners who may compensate us. This may influence which products we write about and where and how they appear on the page. However, opinions expressed here are the author's alone, not those of any bank, credit card issuer, airline or hotel chain. Non-Monetized. The information related to Chase credit cards was collected by Slickdeals and has not been reviewed or provided by the issuer of these products. Product details may vary. Please see issuer website for current information. Slickdeals does not receive commission for these products/cards.

Money loan apps let you borrow cash when you're in a pinch and can't wait until the next paycheck. If you need a small amount of money to cover gas or another purchase, these apps can be a quick and easy way to access funding. But it's important to consider the cost of using these apps compared to other funding options, like a personal loan or a credit card. Some apps do charge unique fees, such as a subscription fee or extra fees for faster funding.

We'll go over your best options for cash advance apps, as well as some other funding alternatives to consider.

8 Best Cash Advance Apps

In this roundup, we've featured our top picks for money loan apps, their standout features, and what you should know.

| App | Loan Amount | Fees | Funding Time |

|---|---|---|---|

|

EarnIn |

Up to $100 per day, $750 per pay period |

No interest or use fees |

Instant |

|

Dave |

Up to $500 |

$1 monthly membership but no interest fees |

Instant, for a fee |

|

Klover |

Up to $200 |

No late or interest fees but express fees are $1.49-$20.78 |

Instant, for a fee |

|

Brigit |

Up to $250 |

$9.99-$14.99 monthly subscription fee but no interest fees |

Instant |

|

Branch |

Up to 50% of earned wages |

No interest or use fees; $2.99-$4.99 for instant external transfers |

Instant |

|

Albert |

Up to $250 |

No late or interest fees |

Instant, for a fee |

|

Empower |

Up to $250 |

$8 monthly subscription fee but no interest or late fees; $1-$8 for instant delivery |

Instant, for a fee |

|

MoneyLion |

Up to $500 |

No cash advance, interest or monthly fees, but $1-$19.99 for other services; $0.49-$8.99 per expedited disbursement |

Instant, for a fee |

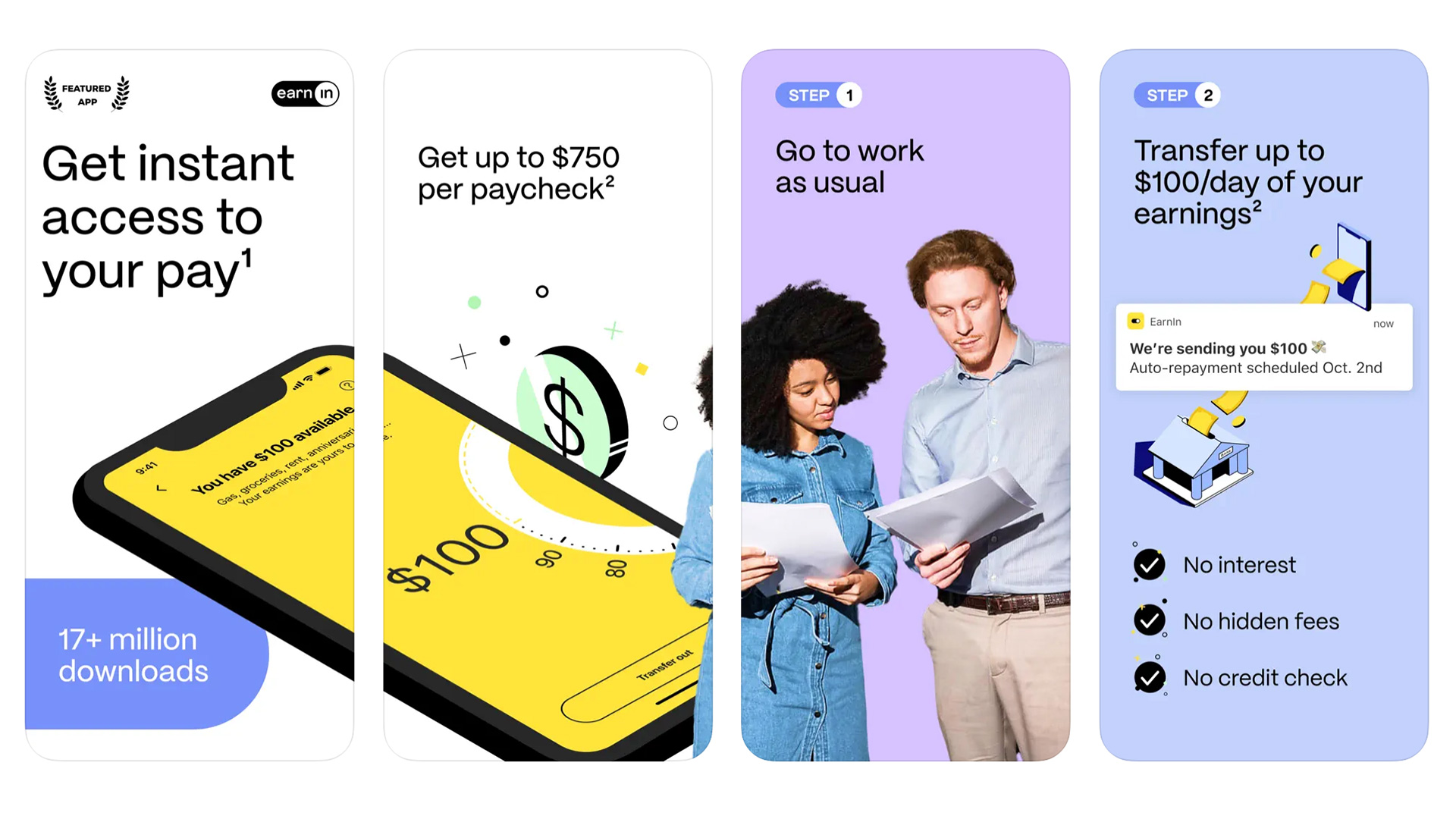

1. EarnIn: Best for Early Paycheck Access

EarnIn

Pros

- No mandatory fees

- No credit check

- Access up to $100 of your pay a day within minutes

- “Boosts” feature can give a temporary pay increase

Cons

- Need a steady payday and pay schedule

- Can only sign up with one employer

Earnin has a spot on our list thanks to its Lightning Speed feature, which can drop cash into your account in minutes (note that fees may apply). You can access up to $100 daily or up to $750 per pay period.

There are technically no fees (you pay back your cash advance when the next payday rolls around), but you can offer an optional tip. A downside is that you need to have a steady pay cycle. Gig economy workers will need to look elsewhere.

Overview:

- How much you can borrow: Up to $100 a day, $750 per pay period

- Price: No cost; tipping is optional

- Fees: No interest fees

- Loans money instantly? Yes

2. Dave: Best for Flexible Repayment

Dave

Pros

- Payment extension available with no late fees

- Budgeting features

- No credit checks

- No interest fees charged

Cons

- Small monthly fee

- Need to open a checking account

There's a lot to love about Dave's cash advance option, such as its easy sign up online, fast cash transfer and no credit checks. But some particularly notable features are its lack of late fees and no interest fees charged, although there are other fees for extra services such as express transfers.

In order to use Dave, you'll need to pay a membership fee of $1 a month and open an ExtraCash account to receive the cash advance.

Overview:

- How much you can borrow: Up to $500

- Price: $1 monthly membership fee

- Fees:

- No interest fees

- Express transfers:

- $3 to $15 for Dave Spending transfers (express)

- $5 to $25 for external transfers

- Loans money instantly? Yes, for a fee

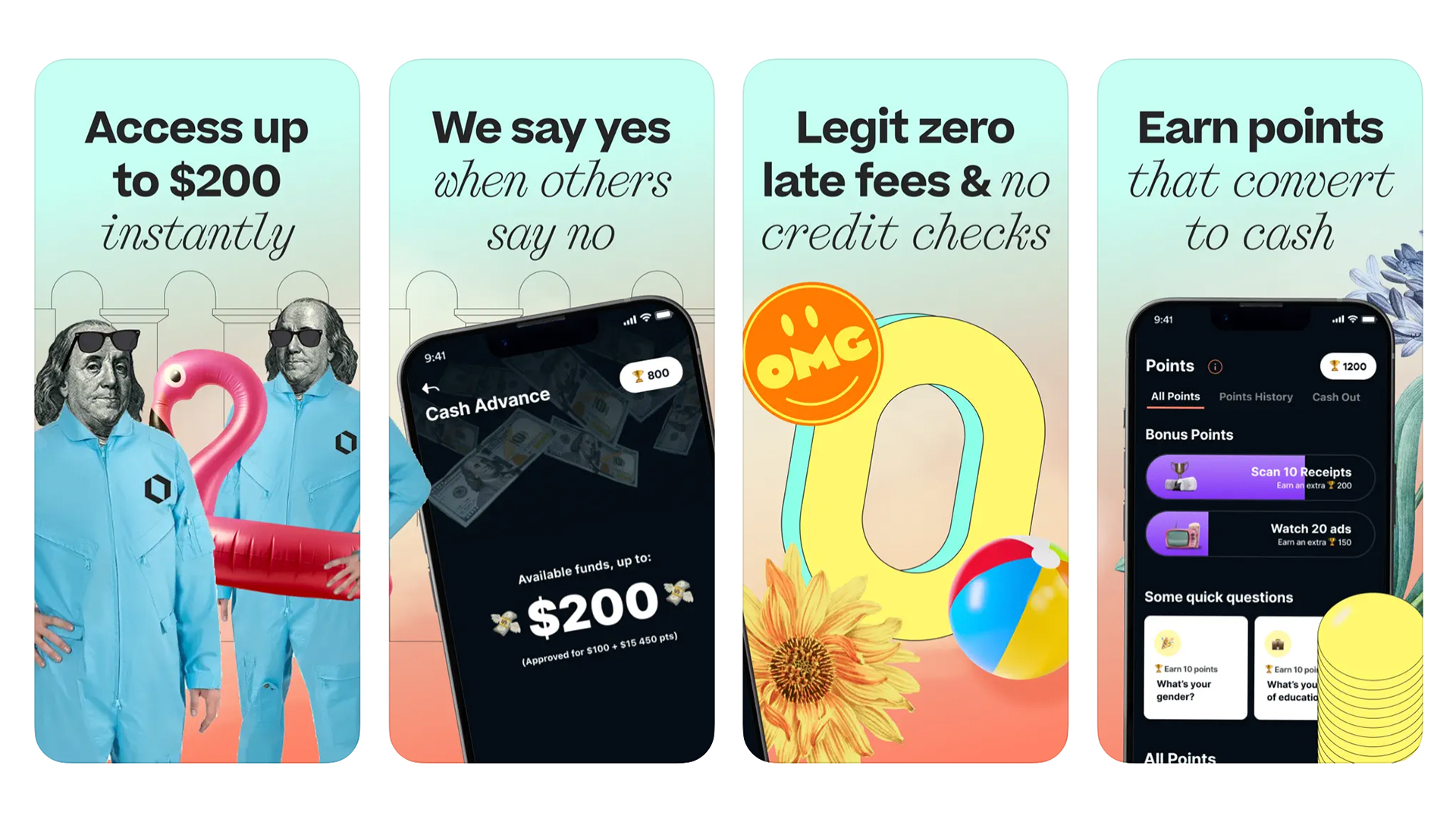

3. Klover: Best for Simplicity

Klover

Pros

- No cash advance or subscription fees

- No credit check

- Quick sign up

Cons

- Can take up to 3 days to get funds

- Express fees can be high

- User data is shared anonymously with third parties

Klover offers a quick and easy way to get up to a $200 cash advance on your paycheck, even if payday is two weeks out. There’s no fee to use the service unless you need the money the same day, in which case you could be shelling out around $20 for the convenience.

The company offers an optional service called Klover+, which provides financial tools like credit monitoring and spending insights. Klover notes that the way it makes money is by selling its users’ data to third parties. The company outlines what it collects and how it shares data in its privacy policy, so it’s worth reading the fine print before you sign up to make sure you’re comfortable with the trade off.

Overview:

- How much you can borrow: Up to $200

- Price:

- Balance advance service: $0

- Optional Klover+: $3.99 per month

- Fees:

- No late or interest fees

- Express fees are $1.49-$20.78, depending on advance amount

- Loans money instantly? Yes, for a fee; otherwise up to three days

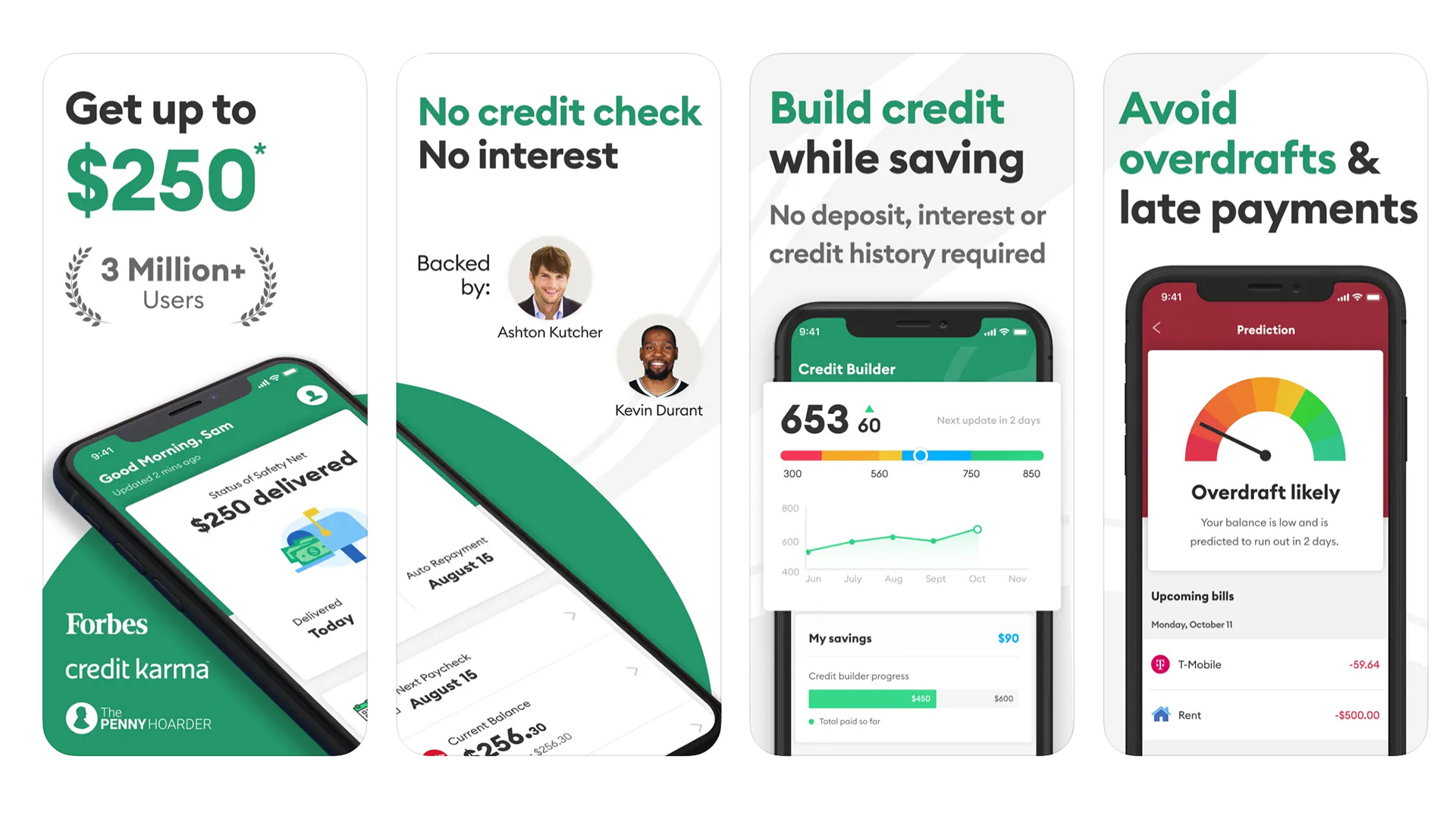

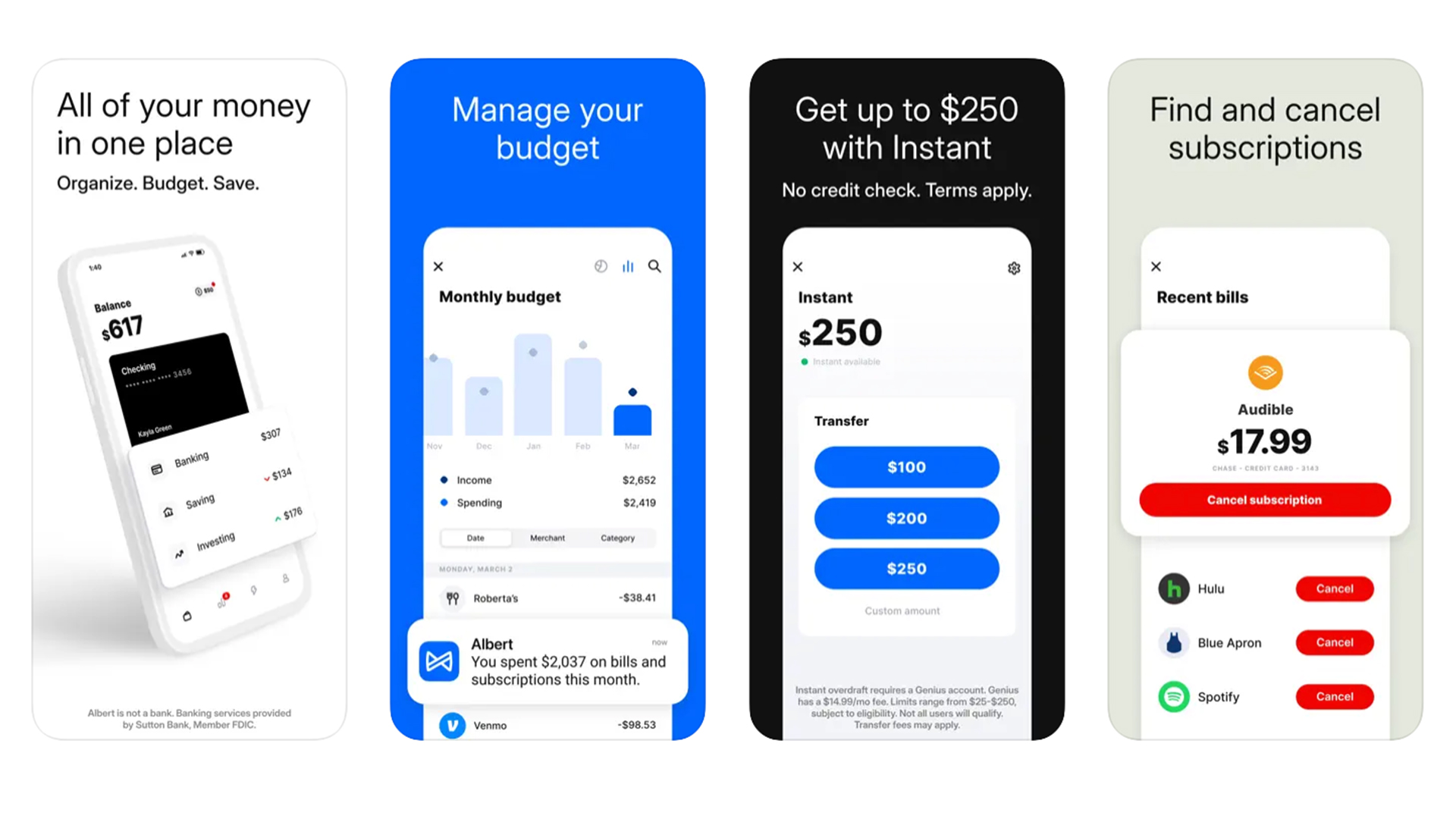

4. Brigit: Best for Budgeting Tools

Brigit

Pros

- Can borrow up to $250

- Get funds instantly

- No credit check

- Builds credit

- No interest fees or late fees

Cons

- Monthly subscription fee of $9.99 to access cash advance with Plus plan

- Need at least three regular deposits from the same employer or source

- Can't ask for an increase in advancement amount

Brigit’s app includes comprehensive, sophisticated budgeting features to help you analyze your spending habits, get alerts on upcoming bills, and receive pointers for improving your finances. Unlike other money loan apps, Brigit reports your payments to the credit bureau to help build credit. Brigit has a free version with a couple features, but to get the most out of the service, you'll need to pay $9.99 or $14.99 per month to access more features.

Overview:

- How much you can borrow: Up to $250

- Price: $9.99 per month for Plus (most services) or $14.99 per month for Premium (all services)

- Fees: No interest fees or late fees

- Loans money instantly? Yes

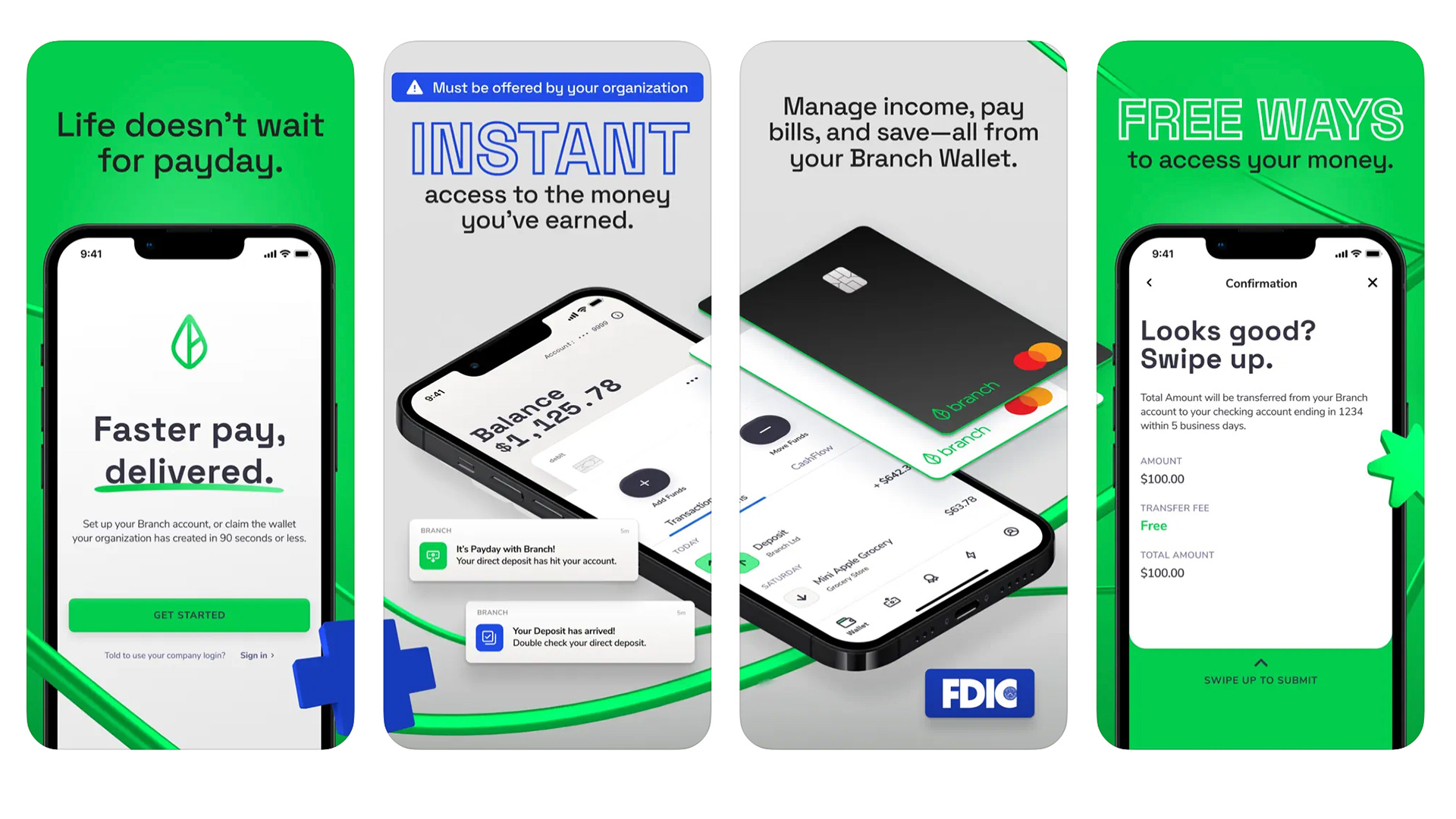

5. Branch: Best for Hourly Workers

Branch

Pros

- Can borrow up to 50% of wages

- Deposit cash from select drugstores and retailers

- Can link up to financial apps to send and receive money

- No interest fees

Cons

- Your employer usually needs to be signed up as a Branch partner

- Fees for instant transfer to an external bank account

With Branch, you can eligible for a payday advance of up to 50% of your paycheck, though there may be a maximum you can borrow at a time. You can receive instant payments after each shift or gig, making it a great choice for independent contractors and gig workers. Branch advance limits are higher than competitors, and you can deposit cash using your Branch branded debit card.

While there are a lot of great perks with Branch, your workplace needs to be a Branch partner to use the app. You can sign up without an employer partnership but expect to jump through hoops and face limitations.

Overview:

- How much you can borrow: Up to 50% of earned wages

- Price: None

- Fees:

- No interest fees

- No fees for instant transfer or 3-day transfer to an external bank account. Fees apply for instant transfer to an external bank account ($2.99 to $4.99, depending on the transfer amount).

- Loans money instantly? Yes

6. Albert: Best for Fintech Fans

Albert

Pros

- No late fees

- No interest

- No credit check

Cons

- Subscription fee required for Instant

- Requires Smart Money feature, which analyzes and invests savings

Albert’s cash advance service is called Instant and essentially works as overdraft coverage up to $250. While basic access to Albert is free, you do have to pony up for a Genius subscription if you want to use Instant, and you have to turn on the app’s Smart Money feature during an active cash advance. Smart Money analyzes your spending and makes investing or savings deposits based on your allocations, which some users may not want. You can, however, turn off Smart Money when you aren’t using Instant.

Albert offers a range of other financial services that could appeal to those who love fintech apps and mobile convenience. Albert Cash is similar to a checking account in that it offers a debit card and is FDIC insured by Sutton Bank. It also provides the opportunity to earn cash back on some purchases. Additionally, the app offers savings, investing and budgeting features.

Overview:

- How much you can borrow: Up to $250

- Price:

- Basic access: $0

- Genius: $12.49-$14.99 per month (required for Instant)

- Fees:

- No late or interest fees for advances

- Instant transfer from Albert Cash to an external bank account is $4.99

- Loans money instantly? Yes, for a fee; otherwise up to three days

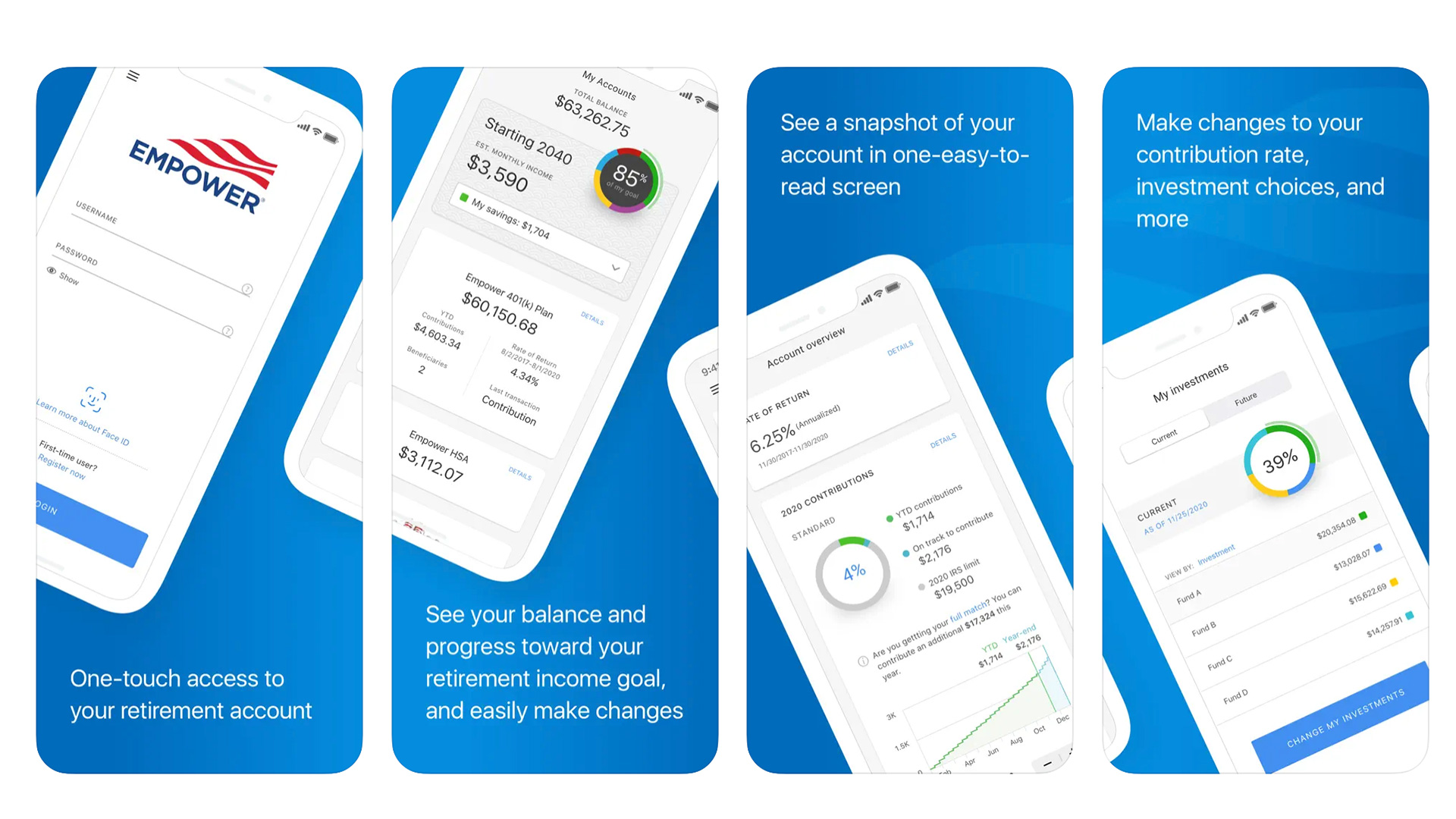

7. Empower: Best for Building Credit

Empower

Pros

- No interest fees or late fees

- Credit monitoring and budgeting tools

- Automated savings account and features

Cons

- Fees for faster delivery

- Relatively low advance amount

- Subscription fee

Empower’s cash advance service doesn’t change interest or late fees, but if you want your money quick, you’ll have to pay for instant delivery. There’s also a monthly subscription fee to use the platform.

The app offers a handful of helpful features in addition to its cash advance service, notably credit monitoring and a savings tool. The app can monitor your financial activity to pinpoint cash you can set aside in the app’s AutoSave account, or you can set a specific time frame to move money there.

Overview:

- How much you can borrow: Up to $250

- Price: $8 per month subscription fee

- Fees:

- No interest fees

- No late fees

- Instant delivery fees are $1-$8, depending on cash advance size

- Loans money instantly? Yes, with fees

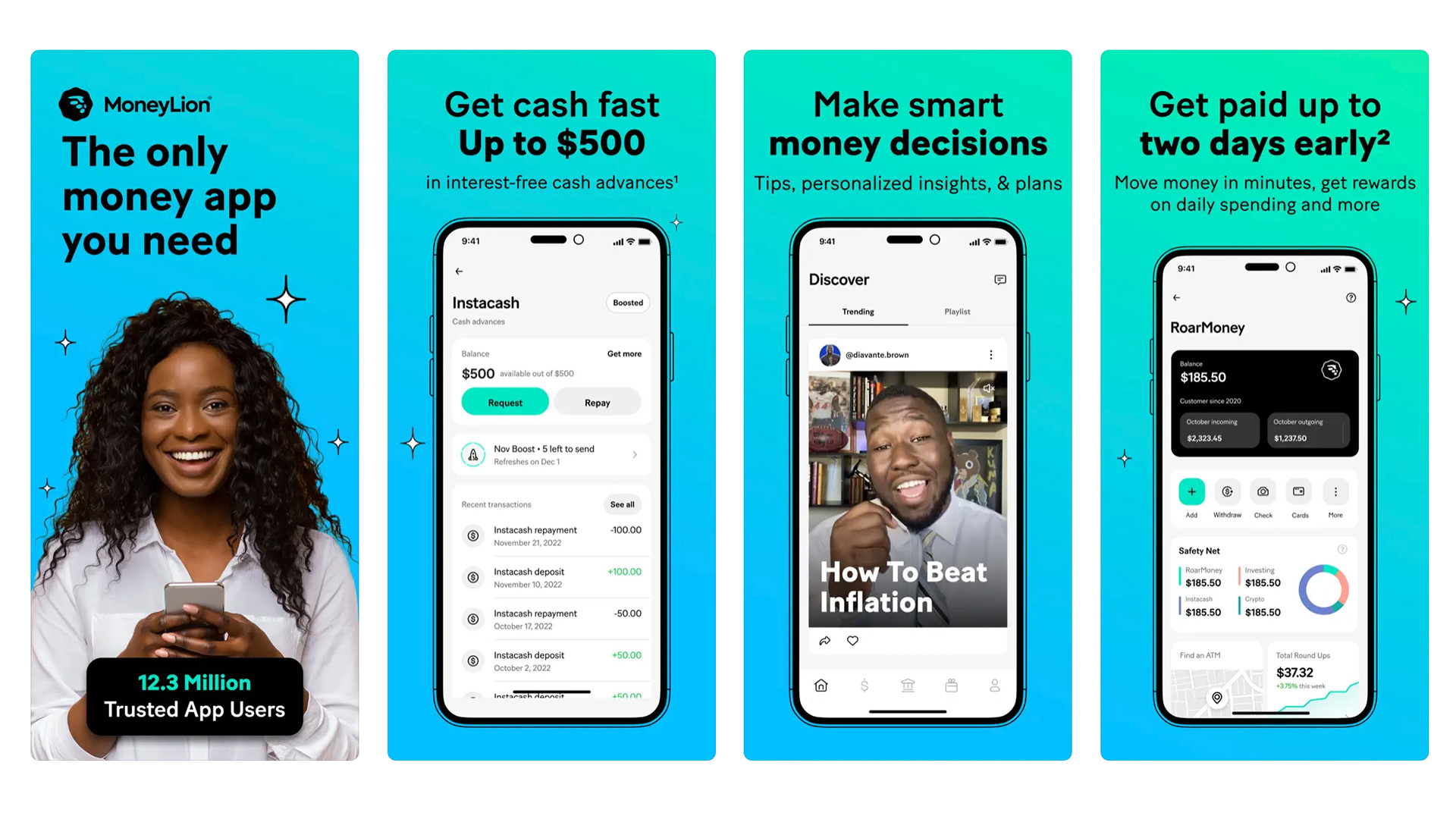

8. MoneyLion: Best for Larger Cash Advances

MoneyLion

Pros

- No interest fees

- Deposit and investment account options

- Credit builder program

Cons

- Steep fees for faster deposit

- Disbursements up to $100 only

- Need history of direct deposit and positive checking account balance to qualify

MoneyLion offers a range of financial services, including an investment account and credit builder program in addition to its cash advance service, which could appeal to people looking to house multiple services under one roof. Instacash, the app’s money loan service, has little in the way of fees unless you need the money fast, in which case you’ll need to pay for the convenience.

Though you can borrow up to $500, MoneyLion disburses funds in $100 increments at most. Regular disbursement can take one to five days, and the longer end of that range is for deposits going outside MoneyLion’s RoarMoney account.

Overview:

- How much you can borrow: Up to $500

- Price: None for cash advance but $1-$19.99 for other services

- Fees:

- No interest fee

- No monthly fee

- Optional expediting fees $0.49 to $8.99 per disbursement increment

- Optional tip

- Loans money instantly? Yes but with fees

Are Money Loan Apps Safe?

When scrambling for fast cash, you might be tempted to jump at the easiest option available for money without any regard for your informational safety. Thankfully, money loan apps use the same security features and technology as banks to protect your financial data, like 256-bit encryption, multifactor authentication, automatic signout and ID verification. They might also require a PIN to sign in and phone verification.

As for making your data available to third parties, each cash advance app has a different policy. It's a good idea to check an app's security and data protection measures before creating an account on one of these platforms.

Alternatives to Cash Advance Apps

If borrowing cash from a money loan app might not be the best choice for you, here are some other options to consider:

Personal Loan

Many online lenders have simple applications, speedy processing times, and larger loan amounts than a money loan app. However, they can’t give you money instantly, and you'll need to pay interest and monthly payments until the loan is paid off. To determine how much you can borrow, use our personal loan calculator.

0% Intro APR Credit Card

If you have great credit, you may qualify for a 0% intro APR credit card, which allows you to make interest-free purchases during the promotional period. As long as you pay off the balance before the promotional time frame, you'll avoid paying interest. But if you carry a balance after that promotional period ends, you'll be facing ultra-high interest rates.

Recommended Balance Transfer Credit Cards

| Credit Card | Intro APR | APR | Rewards Rate | Learn More |

|---|---|---|---|---|

|

|

0% for 21 months on balance transfers and 12 months on purchases

0% Intro APR on balance transfers for 21 months and on purchases for 12 months from date of account opening. After that the variable APR will be 16.49% - 27.24%, based on your creditworthiness. Balance transfers must be completed within 4 months of account opening. |

16.49% - 27.24% (Variable) | N/A |

Apply Now Rates & Fees |

|

|

0% for 18 months on Balance Transfers

Balance Transfer Only Offer: 0% intro APR on Balance Transfers for 18 months. After that, the variable APR will be 17.49% - 27.49%, based on your creditworthiness. |

17.49% - 27.49% (Variable) |

2%Cashback

Earn 2% on every purchase with unlimited 1% cash back when you buy, plus an additional 1% as you pay for those purchases. To earn cash back, pay at least the minimum due on time. Plus, earn 5% total cash back on hotel, car rentals and attractions booked with Citi Travel. |

Apply Now Rates & Fees |

|

|

0% intro APR for 21 months

0% intro APR for 21 months from account opening on purchases and qualifying balance transfers. 17.49%, 23.99%, or 28.24% variable APR thereafter; balance transfers made within 120 days qualify for the intro rate, BT fee of 5%, min: $5. |

17.49%, 23.99%, or 28.24% (Variable) | N/A |

Apply Now Rates and Fees |

|

|

0% intro APR for 12 months

0% intro APR for 12 months from account opening on purchases and qualifying balance transfers. 18.49%, 24.49%, or 28.49% variable APR thereafter; balance transfers made within 120 days qualify for the intro rate and fee of 3% then a BT fee of up to 5%, min: $5. |

18.49%, 24.49%, or 28.49% (Variable) |

2%Cashback

Earn unlimited 2% cash rewards on purchases. |

Apply Now Rates & Fees |

Buy Now, Pay Later (BNPL)

Buy now pay later (BNPL) plans give you a small loan to make an online purchase that you otherwise wouldn't be able to afford. Short-term BNPL loans usually don’t have interest, but you'll need to pay off the loan over four or six installments over a few months to avoid late fees. Longer-term BNPL plans might charge you interest—and the rates tend to be hefty. Opt for too many BNPL plans, and you can easily fall into a debt trap.

Friends and Family Loan

Consider asking a trusted friend or family member if they would loan you money. If you go this route, it’s best to settle on terms and a repayment schedule like you would do with a bank. That way, you can preserve the relationship and avoid unpleasant awkwardness down the line.

Side Hustle

Instead of getting a payday advance or small loan from a cash advance app, pick up a side hustle for extra funds. The small amounts you earn picking up side gigs can help tide you over until the next paycheck. A few hundred extra dollars you earn from dog walking or selling crafty wares on Etsy can be just what you need to cover your bills.

Frequently Asked Questions

-

Money loan and cash advance apps aren't considered payday lenders, but, like payday lenders they come with very high fees. Most money loan apps don't report your payments to the credit bureaus, so they can't impact your credit score one way or the other.

-

Each money loan app features different borrowing limits ranging from $150 per day or between $200 and $250. They're usually smaller amounts than other types of loans. The specific amount you can borrow depends on your situation and how much you're approved for. The lender might bump up this amount if you establish positive financial behaviors, such as making several on-time payments in a row.

-

If a money loan or cash advance app offers you a payday advance, they’ll instantly drop funds into your account. Also, if there's an "instant payment" button, you can receive the funds right away. Money apps that can give you an instant loan include EarnIn, Brigit and Dave.

Jackie Lam

Jackie Lam is a freelance writer with experience covering small business, insurance, budgeting, freelancing and money, and personal finance. Her work has appeared in Salon.com, BuzzFeed, U.S. World & News Report, Time's NextAdvisor, Forbes, and Refinery29. She is an AFC (accredited financial coach) and works with artists, freelancers, and small businesses to improve their relationships with money.